Introduction

Let’s face it: financial planning is like going to the dentist—nobody really wants to do it, but you know it’s necessary. Whether you’re 20, 30, or 60, having a financial plan in place can mean the difference between living comfortably and living paycheck to paycheck. But don’t worry, this isn’t going to be some boring lecture on budgeting. We’re going to take a fun, informal dive into how to navigate your finances through every stage of life, from your wild 20s to your wiser 60s.

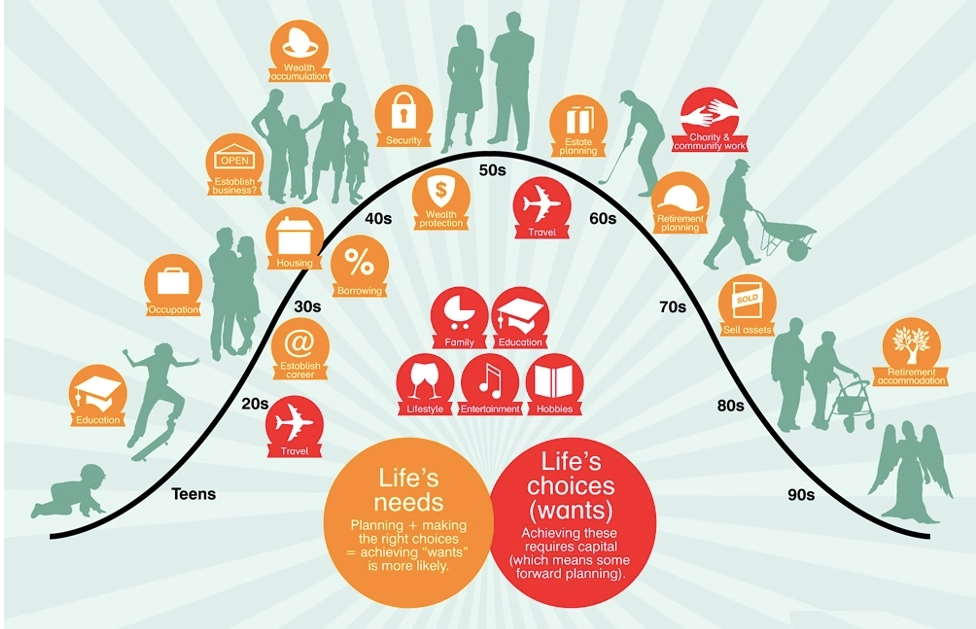

Financial Planning in Your 20s

Ah, your 20s—a time for fun, freedom, and figuring out what the heck you’re doing with your life. Financial planning might not be at the top of your list, but it should be. Why? Because the earlier you start, the more you can take advantage of compound interest (trust me, it’s your best friend). Let’s say you start investing $100 a month at age 25. By the time you’re 65, assuming a 7% annual return, you could have over $264,000. That’s some serious cash for just a little effort!

Besides investing, your 20s are also a great time to build an emergency fund. Life happens—your car breaks down, you lose your job, or you have an unexpected medical bill. Having three to six months’ worth of living expenses saved up can make these setbacks less stressful. And don’t forget about tackling any student loans or credit card debt. The sooner you pay them off, the sooner you can focus on building wealth.

Financial Planning in Your 30s

Welcome to your 30s—the decade where you (hopefully) start to feel more settled in your career and personal life. This is when financial planning gets real. If you’re thinking about buying a house, now’s the time to start saving for a down payment. According to the National Association of Realtors, the average first-time homebuyer is 34 years old, so you’re right on track.

If you’re starting a family, you’ll need to budget for all those adorable (and expensive) baby things. Diapers, daycare, college savings—it adds up fast! Speaking of college, if you plan on helping your kids with tuition, consider opening a 529 plan. It’s a tax-advantaged savings account specifically for education expenses, and the earlier you start, the better.

Your 30s are also a good time to expand your investment portfolio. If you’ve only been investing in stocks, consider diversifying into bonds, real estate, or even starting your own business. Remember, this is the decade where you’re likely earning more, so make sure your money is working as hard as you are.

Financial Planning in Your 40s

Hello, 40s! You’re now in your peak earning years, which means it’s time to really ramp up your savings and investments. If you haven’t already maxed out your retirement accounts, now’s the time to do it. The IRS allows people over 50 to make catch-up contributions to their 401(k) or IRA, which is a great way to boost your retirement savings.

If you have kids, you’re probably thinking about their education. The cost of college has been rising steadily—according to College Board, the average cost of tuition and fees at a private four-year college was over $38,000 in 2023. Yikes! Start saving early, and consider all your options, like scholarships, grants, and student loans.

This is also the decade to pay down any remaining debt, especially your mortgage. The less debt you have going into your 50s and 60s, the more financial freedom you’ll enjoy in retirement. And don’t forget to review your insurance policies—make sure you’re adequately covered, especially if you have dependents.

Financial Planning in Your 50s

Your 50s are all about catching up and getting serious about retirement. If you’re behind on your savings, don’t panic—there’s still time to make up ground. Start by making those catch-up contributions to your retirement accounts. In 2024, the catch-up contribution limit for a 401(k) is $7,500, so take advantage of it!

It’s also a good time to reassess your investment strategy with the help of https://finance-phantom.app/. As you get closer to retirement, you might want to shift your focus from growth to preservation. This means reducing your exposure to riskier investments like stocks and increasing your holdings in bonds or other safer options.

Healthcare costs are another big consideration. According to Fidelity, the average couple retiring at 65 in 2023 will need about $300,000 to cover healthcare expenses in retirement. If you have a Health Savings Account (HSA), now’s the time to beef it up. HSAs offer triple tax advantages—your contributions are tax-deductible, the money grows tax-free, and withdrawals for medical expenses are tax-free.

Financial Planning in Your 60s

Congratulations, you’ve made it to your 60s! Retirement is on the horizon, and it’s time to start planning for the big day. One of the first things to consider is your withdrawal strategy. How will you take money out of your retirement accounts without running out? The 4% rule is a popular guideline—it suggests withdrawing 4% of your retirement savings each year. But remember, everyone’s situation is different, so consult a financial advisor.

Social Security is another big piece of the puzzle. You can start taking benefits as early as 62, but your monthly check will be larger if you wait until your full retirement age (which is 67 for those born in 1960 or later). Deciding when to take Social Security is a big decision, so weigh your options carefully.

Finally, don’t forget about estate planning. This includes writing a will, setting up a trust, and designating beneficiaries for your accounts. It might not be the most fun topic to think about, but it’s crucial to ensuring your loved ones are taken care of.

Common Financial Planning Mistakes at Each Stage

Let’s take a quick detour to talk about some common mistakes people make at each stage of life. In your 20s and 30s, overspending and not saving enough for retirement are biggies. In your 40s and 50s, it’s ignoring your retirement accounts or not paying down debt fast enough. And in your 60s, it’s not having a solid withdrawal strategy or estate plan in place. The good news is, by being aware of these pitfalls, you can avoid them.

Adjusting Your Financial Plan Over Time

Life is full of surprises, and your financial plan should be flexible enough to adapt. Whether it’s marriage, divorce, the birth of a child, or a career change, these milestones will impact your finances. That’s why it’s essential to regularly check in on your plan and make adjustments as needed. For example, if the market takes a downturn, you might need to rebalance your portfolio to protect your assets.

The Role of Insurance at Different Life Stages

Insurance might not be the most exciting topic, but it’s a crucial part of your financial plan. In your 20s and 30s, health and life insurance are must-haves. As you enter your 50s and beyond, consider long-term care insurance to cover potential healthcare costs down the road. And don’t forget about disability insurance, which can protect your income if you’re unable to work.

Investing Wisely at Every Stage

Investing isn’t a one-size-fits-all strategy—it should evolve as you age. In your 20s, you can afford to take more risks with stocks because you have time to recover from any losses. But as you get older, it’s wise to shift towards more conservative investments like bonds. Target-date funds are a great option because they automatically adjust your asset allocation based on your age.

The Psychological Aspects of Financial Planning

Let’s not forget the psychological side of money. Financial security isn’t just about dollars and cents—it’s about peace of mind. Studies have shown that financial stress can lead to anxiety, depression, and even physical health problems. By having a solid financial plan in place, you can reduce stress and focus on enjoying life, no matter what stage you’re in.